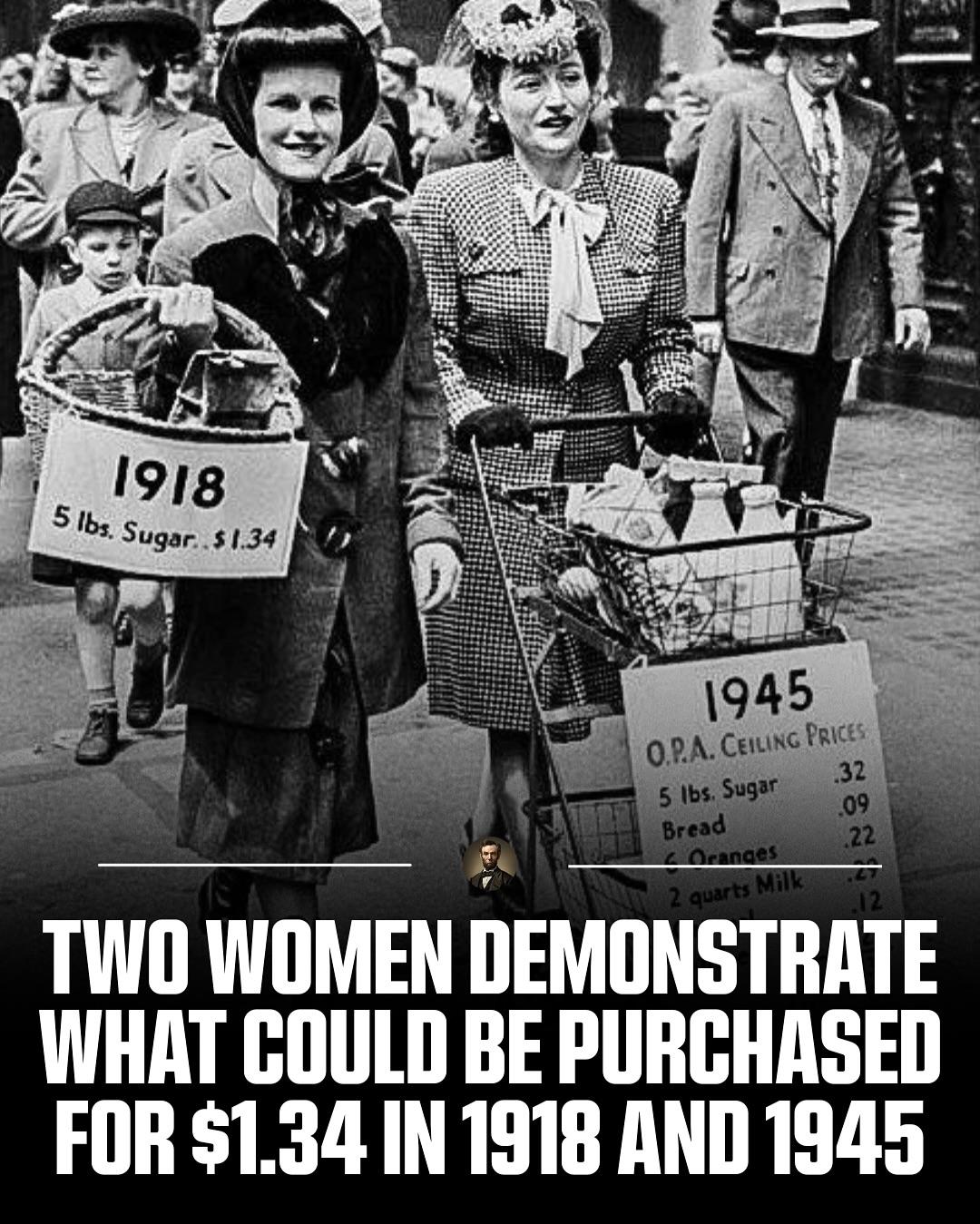

Buying a home is often seen as one of the biggest financial milestones in life, but most people don’t realize how much they actually end up paying for that house over the life of the loan. Let’s take an example: a $250,000 home with a small 3.5 percent down payment of $8,750. That leaves a loan amount of $241,250. At an interest rate of 6.5 percent over 30 years, the numbers get shocking. The total interest paid comes out to $307,701.08. That is more than the cost of the house itself. Adding in the original loan balance of $241,250, the total amount paid over 30 years is $548,951.08.

This shows why understanding how interest works is so critical in personal finance. The sticker price of the house is not the true cost. The mortgage terms, interest rate, and loan length all play huge roles in how much wealth you keep versus how much you hand over to the bank. Homeownership can absolutely be a wealth building tool, but only if you manage it wisely. Paying extra toward the principal, refinancing for a better rate, or shortening the loan term are strategies that can save you tens of thousands of dollars.

Wealthy people understand that every dollar saved in interest is a dollar that can be invested elsewhere. Imagine if even a portion of that $307,701.08 in interest was instead invested into the stock market over 30 years. With compound growth, it could easily turn into millions. That is why managing debt is just as important as learning how to invest. True wealth building comes from keeping more of your money working for you instead of letting it slip away in interest payments.

If you want to see how I personally invest and manage my portfolio, comment “Stocks” and I’ll share it with you.

Would you rather pay off your mortgage early and save on interest or invest extra cash while keeping the loan?

Follow @MasteringWealth for more insights on personal finance, investing, and strategies to help you grow wealth and make smarter money moves.

Disclaimer: This content is for educational purposes only and is not financial advice. Always do your own research before making financial decisions.

Buying a home is often seen as one of the biggest financial milestones in life, but most people don’t realize how much they actually end up paying for that house over the life of the loan. 🏡 Let’s take an example: a $250,000 home with a small 3.5 percent down payment of $8,750. That leaves a loan amount of $241,250. At an interest rate of 6.5 percent over 30 years, the numbers get shocking. The total interest paid comes out to $307,701.08. That is more than the cost of the house itself. Adding in the original loan balance of $241,250, the total amount paid over 30 years is $548,951.08. 💸

This shows why understanding how interest works is so critical in personal finance. The sticker price of the house is not the true cost. The mortgage terms, interest rate, and loan length all play huge roles in how much wealth you keep versus how much you hand over to the bank. Homeownership can absolutely be a wealth building tool, but only if you manage it wisely. Paying extra toward the principal, refinancing for a better rate, or shortening the loan term are strategies that can save you tens of thousands of dollars. 🏦

Wealthy people understand that every dollar saved in interest is a dollar that can be invested elsewhere. Imagine if even a portion of that $307,701.08 in interest was instead invested into the stock market over 30 years. With compound growth, it could easily turn into millions. That is why managing debt is just as important as learning how to invest. True wealth building comes from keeping more of your money working for you instead of letting it slip away in interest payments. 📈

If you want to see how I personally invest and manage my portfolio, comment “Stocks” and I’ll share it with you. 📩

Would you rather pay off your mortgage early and save on interest or invest extra cash while keeping the loan? 🤔

Follow @MasteringWealth for more insights on personal finance, investing, and strategies to help you grow wealth and make smarter money moves. 🚀

Disclaimer: This content is for educational purposes only and is not financial advice. Always do your own research before making financial decisions.